Medicare Part D Basics

Today’s video is on Medicare Part D, Medicare’s outpatient drug benefit. Please watch the video.

Medicare Part D began in 2006, 40 years after original Medicare started. The long delay in adding drug coverage to Medicare was due to concern that the country could not afford a Medicare outpatient drug benefit as is evidenced by the rather odd plan design of Part D.

Medicare Part D is an often-maligned benefit for several reasons. The coverage is not as rich as one would find in a generous corporate plan, plan design is complex, and shopping for coverage is somewhat challenging because of the number of plan options from which one can choose. We should never forget, however, how important and how valuable a protection Part D is. We recommend everyone who is on original Medicare or on an Advantage Plan that does not include drug coverage, enroll in a Part D Plan. You’ll pay a penalty if you don’t enroll when you are first eligible but, more important, everyone needs the protection of drug coverage.

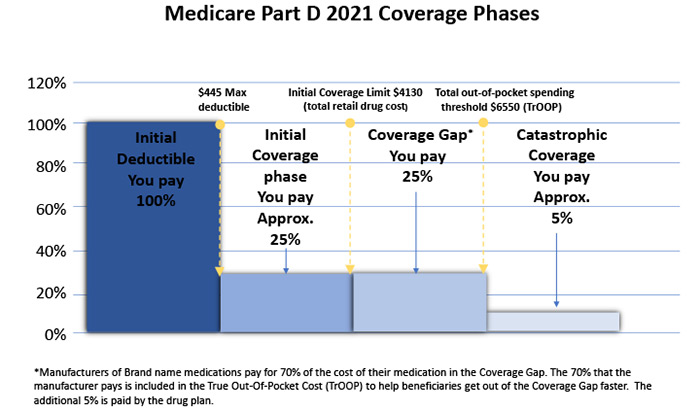

Part D Plans are administered by private companies and there are typically around 25 plans to choose from in a given metropolitan area. Every year the federal government sets how high a deductible Part D plans can have. In 2021, the maximum deductible is $445 but there are plans with no deductible and plans with deductibles below the $445 maximum.

The Part D benefit design is illustrated in the chart above. After meeting your deductible, you are in the Initial Coverage Phase where you pay about 25% of the cost of your drug. However, some Plans will choose to cover inexpensive generics with no copayment or coinsurance during the deductible and Initial Coverage Phase. When what you have paid and what your Plan has paid together reaches $4,130, you enter the Coverage Gap Phase. Coverage in the Coverage Gap is, thankfully, better than it used to be when this phase was the dreaded “donut hole” and one’s benefit was much less than the Initial Coverage Phase. Some medications can even be less expensive in the Coverage Gap than in the Initial Coverage Phase. Nevertheless, it can still be unnerving to face payments for a drug that can change over the course of a year when so many people are expecting a consistent out-of-pocket amount. The coinsurance can be modest in such instances but the process can seem bewildering.

Once you have spent $6,550 on drugs in 2021, you have reached the Catastrophic Coverage Phase and coinsurance should be about 5% for the remainder of the calendar year. This process then resets every January 1. There is no out-of-pocket maximum with Medicare Part D plans.

Sometimes, if a drug isn’t covered by your drug plan, you might consider using a discount coupon as discussed in a previous video. Generally, however, you want to obtain all your drugs through your Part D plan, and if a drug isn’t covered by your plan, request a formulary exception or appeal.

You can change Part D plans every year during the annual enrollment period of October 15th through December 7th. Like Advantage Plans, Part D plans are associated with your primary residence so you must plan ahead if you anticipate moving.

Medicare Part D is a very important financial protection. Thanks for learning more about it.